Governing Agentic AI in Insurance: From Principles to Operating Model

Insurance governance for agentic AI must move beyond static principles and model review toward runtime workflow governance, controlled execution, and an operating model that connects business intent, technical controls, and regulator readiness.

EXECUTIVE SUMMARY

Shift to Runtime Governance: Move beyond static, pre-deployment model reviews to active, continuous monitoring of AI agents within live decision workflows.

System-Level Risk Management: Recognize that risk resides not just in the AI model itself, but in the entire workflow, including data access, automated actions, and human-in-the-loop oversight.

Built-In Transparency: Automate the generation of audit logs, control evidence, and compliance documentation directly within the operational process to satisfy evolving regulatory demands.

Introduction

Insurance is becoming one of the clearest tests of whether artificial intelligence can be governed in production. The issue is no longer simply whether AI can generate useful outputs, but whether AI-driven decisions can be controlled, explained, monitored, and scaled across underwriting, claims, servicing, fraud, and adjacent workflows.

That challenge is especially acute in insurance because decisions are high-volume, high-impact, and deeply connected to customer outcomes, regulatory obligations, operational risk, and enterprise accountability. In this environment, governance cannot remain a static policy exercise or a one-time model review. It must become part of the architecture of execution itself.

This is the core shift now facing carriers. The next phase of insurance AI will be defined less by model novelty and more by governance maturity: the ability to operationalize controls, human oversight, evidence generation, and continuous assurance inside the flow of live decision-making. Consider the deployment of an AI agent for initial claims triage: if the agent automatically fast-tracks a claim or routes it to a special investigations unit (SIU), the insurer must be able to prove exactly which data points triggered the decision and demonstrate that the outcome was free from historical bias.

Why Insurance Requires a Different Governance Model

Insurance has always been a business of judgment under constraint. Carriers must make decisions quickly, but they must also ensure those decisions are fair, defensible, explainable, and aligned with business and regulatory requirements.

That is why generic AI governance models are often insufficient on their own. Insurance workflows span multiple systems, data sources, handoffs, and lines of accountability. For example, a commercial underwriting workflow might involve drawing data from property databases, parsing unstructured submission documents, and applying carrier-specific risk guidelines. The actual risk does not sit only in the language model extracting the data; it sits in the full decision system: the data it uses, the workflow it enters, the actions it triggers, the exceptions it creates, and the evidence it leaves behind.

A stronger governance approach for insurance therefore begins with a simple recognition: governance is not just model governance. It is workflow governance, decision governance, and operating-model governance.

Principles Are Necessary but Not Enough

Most carriers already understand the language of trustworthy AI. Fairness, explainability, accountability, security, and human oversight are now well established as governance principles across the market.

But principles do not create operational control on their own. They become meaningful only when they are translated into system design, workflow policy, escalation logic, monitoring, and evidence generation. This aligns with the direction of modern AI risk management frameworks, which emphasize continuous measurement and management over one-time reviews.

For insurance, this means the governance conversation has to move beyond statements of intent. The real question is how principles become enforceable in production. A commitment to "fairness" must translate into a specific workflow control, such as an automated parity check before a pricing decision is finalized, or a mandatory human review threshold for coverage denials.

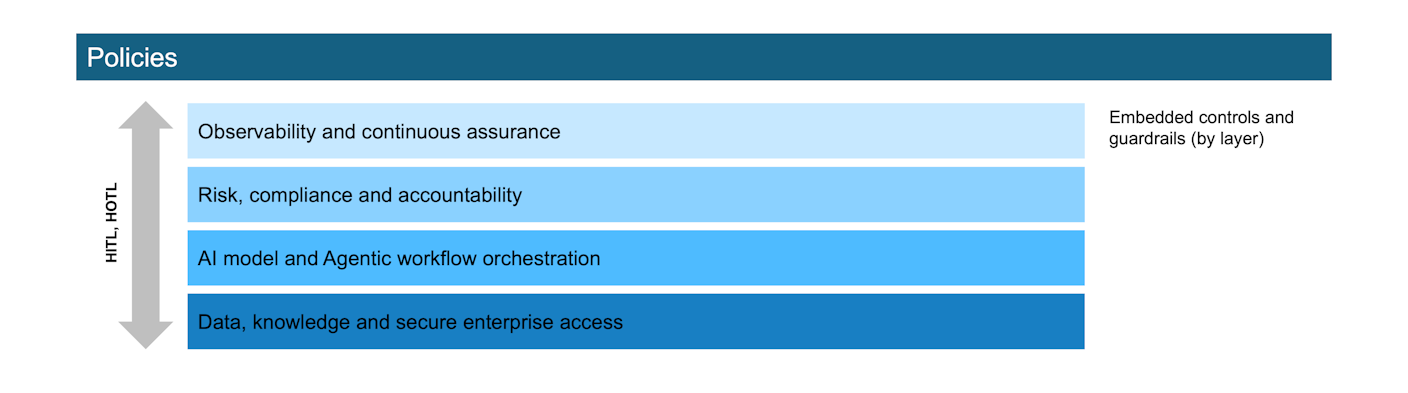

A Governance Operating Model for Agentic Insurance

A practical operating model for agentic insurance should be multilayered, ensuring that strategic intent seamlessly translates into technical execution.

Strategy Layer. Governance at this level aligns AI initiatives to business priorities and risk appetite. It provides clear definitions of which decisions- such as routine policy endorsements- may be fully automated, and which, like complex liability determinations, must be reserved for human judgment.

Workflow Layer. This layer defines how agents, models, and people interact across specific processes. It maps the orchestration of tasks, such as how an AI underwriting assistant summarizes a submission, highlights missing information, and routes it to a human underwriter for final approval.

Control Layer. The control layer specifies granular technical parameters: what enterprise data an agent can access, what downstream systems it can update, when escalation is strictly required, and what audit artifacts must be captured during the transaction.

Governance operating model

A simple view of how business intent, workflow orchestration, and runtime controls fit together in an insurance-grade agentic operating model.

A strong operating model also requires technical and operational disciplines that work together: secure enterprise data access, workflow and agent orchestration, version control, model and prompt management, role-based permissions, observability, and policy enforcement. In this sense, governance is not a review gate sitting outside the system. It is part of the system design.

“In insurance, the governance challenge is no longer just model risk. It is decision-system risk.”

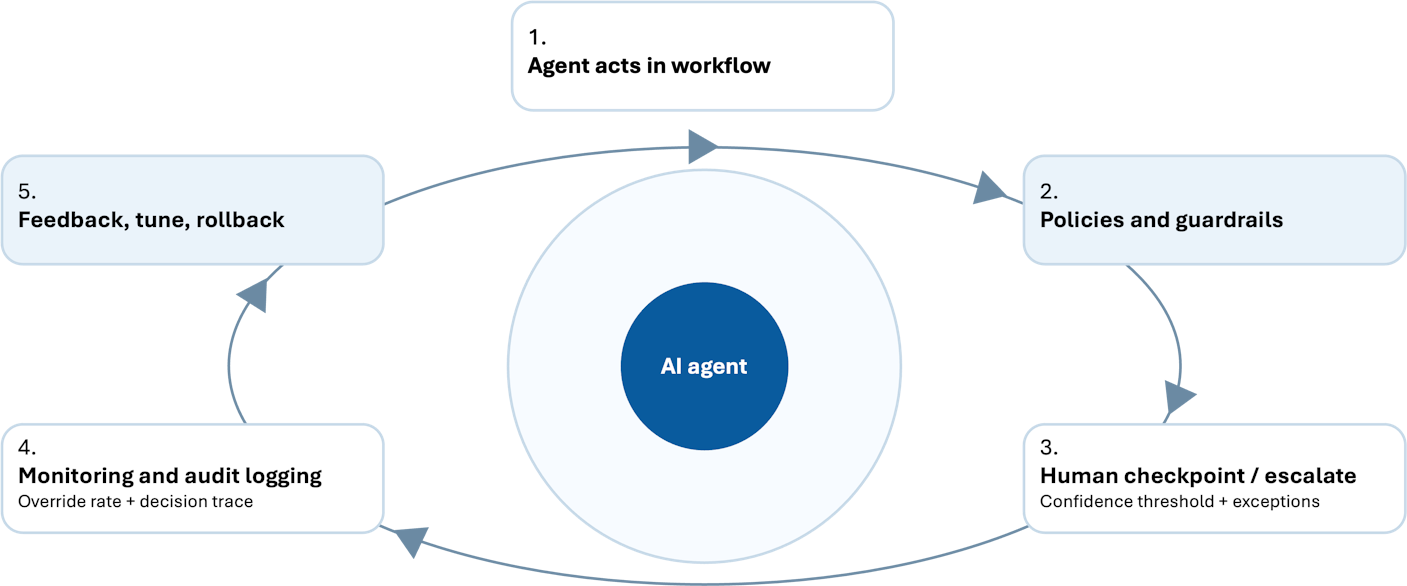

Runtime Governance, Not Static Assessment

One of the most important shifts in agentic insurance is the move from static assessment to runtime governance. Traditional controls often focus on pre-deployment validation, documentation, and approval. Those remain necessary, but they are no longer sufficient when AI participates in live workflows that change with data, context, and business conditions.

A more resilient model requires continuous monitoring and control. In practice, that can include policy-as-code, prompt and injection safeguards, access restrictions, fairness checks, drift detection, escalation paths, rollback triggers, and live audit logging tied directly to execution events. For example, if an AI agent is drafting customer communications, runtime governance ensures that a human-in-the-loop (HITL) checkpoint is triggered if the model's confidence score drops below a predefined threshold.

This is where mature governance becomes measurable. Instead of asking only whether a model passed review, carriers can ask whether a governed workflow is behaving within tolerance, whether human override rates are rising, whether exceptions are increasing, whether explanations remain usable, and whether the system is producing evidence that risk and compliance functions can trust.

Runtime governance control loop

Runtime governance turns live execution into a monitored, traceable feedback cycle rather than a one-time approval event.

Transparency, Auditability, and Regulator Readiness

For insurers, transparency is not a communications exercise. It is an operational requirement.

As AI becomes more embedded in core decisions, carriers need explainability narratives, model and workflow documentation, audit logs, control evidence, and regulatory mappings that are generated as part of the operating process. Those artifacts should not be assembled manually at the end of a project or in response to a market conduct exam. They should be produced continuously as part of how the system runs.

This matters because regulatory expectations are moving toward stronger documentation, structured risk assessment, human oversight, and demonstrable control effectiveness.

Authorities are increasingly focusing on AI uses that affect economically significant decisions. A carrier-ready governance model must therefore automatically generate comprehensive compliance evidence- such as decision traceability logs and dynamic model cards- to prove that human oversight was applied appropriately.

How Carriers Should Start

Most insurers should not attempt to govern every AI use case at once. A more practical path is to start with one bounded workflow where speed, consistency, and accountability all matter, then build the governance model around that workflow from day one.

Select a bounded, high-value workflow. Begin with a specific process that has clear decision boundaries, such as a first-notice-of-loss (FNOL) data extraction or an underwriting workbench expansion, rather than a generalized enterprise rollout.

Define the AI's operational boundaries. Explicitly map out where the AI agent is authorized to support, recommend, act, or escalate based on predefined business rules.

Establish human-in-the-loop design. Designate clear intervention points for human experts, ensuring sensitive or high-impact decisions always require human authorization before final execution.

Instrument for monitoring and evidence. Implement comprehensive logging, exception handling, and compliance mapping within the workflow, ensuring all controls and evidence requirements are met before scaling to the next process.

This phased approach allows the organization to prove not only that AI can improve throughput, but that governed execution can scale without creating unmanageable control debt.

Conclusion

Insurance does not need more abstract AI principles in isolation. It needs a governance operating model that can make principles enforceable inside real workflows.

The firms that lead in agentic insurance will not simply be the ones with the most pilots or the most advanced models. They will be the ones that can connect business intent, technical controls, human judgment, and regulatory evidence into one governed execution layer.

That is the real opportunity. When governance is embedded into execution rather than added afterward, carriers can move from experimentation to scalable adoption with greater confidence, clearer accountability, and stronger institutional trust.

Header photo by rawpixel.com / George

Related content

Post / The next frontier of insurance AI: workplace orchestration

Insurance advantage will come from building an agentic Workplace where AI and people redesign how underwriting and claims work gets done.

Post / AI’s Sweet Spot with the GenAI Scorecard

A comprehensive scorecard helps organizations to evaluate the performance and impact of GenAI solutions regularly.

Post / Transforming Insurance with Generative AI

Unlock the power of Generative AI in insurance distribution for personalized service and enhanced efficiency.

Subscribe to Our Newsletter

Get the latest insights about Global solutions for leading insurers on your email